For all the pain and suffering COVID-19 has inflicted and will inflict before it subsides, it has also created a historic opportunity to pivot toward a green economy. The “pandemic pause” has created a window to stop and think about where we want to go when this is over. This seven-part Corporate Knights series of articles and online roundtables has explored how to make the coming economic recovery one that leapfrogs us forward in the quest for a calmer, cooler climate and peace with nature.

It has been clear for some time that our economy is on a collision course with the natural ecosystems it’s dependent upon. Thankfully, there’s a large and accelerating body of know-how when it comes to the changes that need to happen to get to zero carbon. For every one of the amazingly talented and wise panellists who have participated in these roundtables, there are hundreds more who are focused on this transition. With the pandemic-triggered prospect of renewed public investment, and with the creative leadership up-and-coming generations bring to the game, a door has opened. We have tried in this series to give a glimpse of what awaits us over the threshold.

By 2030, Canada could create more than five million quality job-years of employment by greening the power grid, electrifying transport and upgrading our homes and workplaces to be more comfortable and flood resilient. This wouldn’t just be good for jobs – it’s a pocketbook issue that would save Canadians a lot of money: $39 billion per year at the pumps and on heating and power bills by 2030 (in today’s dollars).

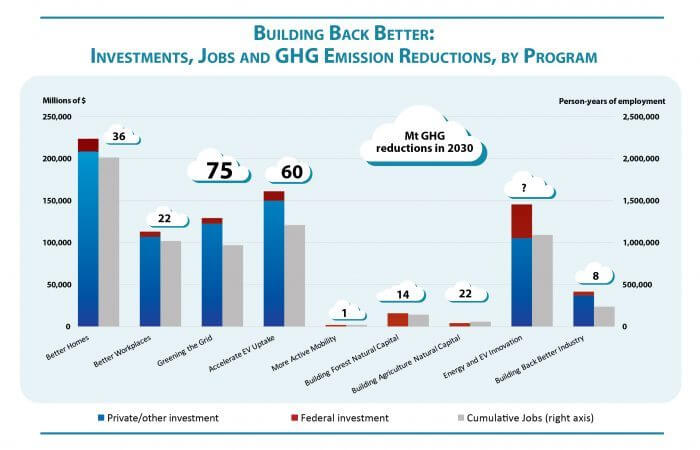

Note for chart below:Investment is Millions of $ total to 2030, and Person-years of employment is total to 2030.

We could also help to protect more than a million jobs that are at risk by:

● offering rebates for low-carbon cement, steel and mass timber,

● supporting farmers to adopt practices and technologies for restoring the soil while paying them fairly for the ecosystem services they provide,

● paying young people to plant an extra 800 million trees per year and supporting Indigenous communities to be forest guardians, and

● providing seed investment with an Natural Resources and EV Innovation Fund (which could be administered by existing institutions) to catalyze Canadian champions in fast-growing industries of the future where we have competitive advantages (lightweight bitumen-based carbon fibres, renewable jet fuels, green hydrogen, batteries and electric vehicles).

In the wake of the COVID crisis, in which more than three million Canadians have lost their jobs, this is all within reach if we choose to build back better by making these job-rich themes a priority in the federal government’s stimulus and recovery packages.

Making this happen would require a federal investment of $10 billion per year (0.4% of GDP) on average over the next decade. Forty percent of this total would be front-loaded in the first two years as part of the stimulus/recovery package, with strings attached to ensure essential complementary policies in other jurisdictions, including net-zero building codes for new and existing buildings by 2022, fair power-grid access for storage and renewables, and an electric vehicle mandate for Canada. To keep the momentum going, additional non-grant federal financial support would be offered, including in the form of low-cost loans and guarantees.

Underpinning all of this would be investment in skills training so that Canadians learn while they are working in these new jobs. We have done this before. When teachers were urgently needed for the new public education system early in the 20th century, they were given intensive training for one year followed by years of in-service training during their early careers. These teachers were a vital part of Canada’s nation building as we recovered from the ravages of war and a pandemic.

Over a decade, the federal investment in the programs we have proposed would total $106 billion, crowding in an additional $681 billion in private and other sector investment, creating 6.7 million years of employment – more than twice the jobs that have been lost due to COVID-19. These investments would reduce greenhouse gas emissions by an estimated 237 million tonnes from 2018 levels. That would meet our Paris Climate Agreement commitments and put us on a path to a carbon-free economy within a generation.

These investments are of the same order of magnitude as those being made in Canada today. Case in point: the deep retrofits to homes required to make them more comfortable, cheaper to heat and cool, and better prepared to withstand floods and extreme weather works out to about $20 billion per year. That’s just one-third the $60 billion Canadians spend on home renovations each year. Similarly, the investments to decarbonize Canada’s transmission grid are on par with business-as-usual investments happening today.

Support for a green recovery is mounting.

Some of the world’s leading economists recently completed an analysis of possible COVID-19 economic recovery packages. They concluded that green projects create more jobs, deliver higher short-term economic returns per dollar spent and lead to increased long-term cost savings, compared to traditional fiscal stimulus.

This finding is also supported by McKinsey’s research, which found a low-carbon recovery could not only initiate the significant emissions reductions needed to halt climate change but also create more jobs and economic growth than a high-carbon recovery would. Our proposals are very much in line with this research.

Canadians want to do this.

In an Ipsos global poll, 61% of Canadians said they agree or tend to agree that “in the economic recovery after COVID-19, it’s important that government actions prioritize climate change.” And that was without being given information about the jobs-rich nature of a green recovery.

Other countries are reaching the same conclusions we have:

● On May 27, the European Commission proposed a €750 billion ($1.137 trillion) recovery fund to steer the continent toward carbon neutrality by 2050, with a quarter of the plan earmarked for climate action.

● On May 26, France announced an €8 billion ($12 billion) plan to accelerate the transition to electric cars, which will include increasing the amount buyers can receive as a state incentive toward the purchase of an electric car.

● German Chancellor Angela Merkel has indicated that her government aims to implement a stimulus package that “helps the economy’s move toward climate neutrality,” saying “it will be all the more important that if we set up economic stimulus programs, we must always keep a close eye on climate protection.”

● Denmark has allocated 30 billion kroner ($6 billion) for green building renovations, estimated to help upgrade 72,000 homes.

How to pay for it?

The federal investment component of this could be financed via green bonds, but we don’t need to take on additional debt to do this. We can find the money for the public investments needed to seize this opportunity by making minor and long-overdue changes to Canada’s tax code.

According to Finance Canada, there are more than 170 corporate tax giveaways that add up to more than $156 billion per year. While some have public benefit (such as small business supports, charitable deductions for corporations, R&D tax credits and regional assistance funds), there are at least five naked examples of corporate welfare that sap more than $40 billion dollars from the public purse every single year with little to show for it – and that’s not even counting the billions of dollars siphoned off each year via elaborate corporate tax-avoidance schemes.

In addition, the Canada Revenue Agency estimates that tax avoidance by roughly 15,000 large corporations is costing Canada 6.7 to $7.9 billion per year, but that’s a low-ball estimate. A six-month investigative analysis by the Toronto Star, Corporate Knights and Paul Rhodes, an International Financial Reporting Standards (IFRS) expert, found that the 100 largest companies in Canada avoided $62.9 billion in taxes over a six-year period, for an average of $10.5 billion per year.

That’s the same amount of public investment that’s needed to catalyze the Building Back Better program to crowd in $730 billion in private investment, create 6.7 million years of employment and deliver $39 billion annually in savings to Canadians, all the while putting us well on the path to net-zero emissions by 2050.

Why don’t we plug those holes and invest a fraction of the money on a temporary basis to build back better and catalyze the industries of the future that preserve rather than plunder our planet, while creating 6.3 million quality jobs?

If timing and political constraints don’t allow for the tax reform measures, with its AAA sovereign bond rating Canada could issue a green bond with proceeds ring-fenced for green recovery purposes and regular reporting on the use of proceeds. It would send a signal to global investors that Canada is serious about reaching net-zero emissions by 2050 and halving its emissions by 2030.

The institutions that will enable the investments in the Building Back Better program are ready and capable of doing this today. After the Second World War, the CMHC (then known as the Central Mortgage and Housing Corporation), in partnership with Canadian chartered banks, led the way in helping to house Canadians. Now the CMHC can lead in transforming Canadian homes and workplaces into more valuable, functional and comfortable buildings that have been deeply retrofitted.

Similarly, the Canada Infrastructure Bank is ready to invest in transmission infrastructure that will underpin a $100 billion investment in Canada’s sun and wind belt in Alberta and Saskatchewan that would put Canada at the forefront of 21st-century grid technology.

Canada also has strong institutions for energy innovation and economic diversification. Over the past century, Natural Resources Canada has successfully funded energy research, development and demonstration, as has Innovation, Science and Economic Development Canada in economic diversification. And Export Development Canada has the mechanisms in place to assure multi-year commitments, including through loan programs to corporations of all sizes (and a new program of guaranteed loans to support oil and gas companies that could be extended to the green industries of the future). The Invest in Canada program, set up to support economic prosperity and stimulate innovation in Canada, can also play a role in attracting investment in the fast-growing industries of the future that play to Canada’s natural advantages.

And there are many capable provincial agencies with strong technical capacity that can act as vehicles to carry out the R&D and pilots we have proposed, including Alberta Innovates, Emissions Reduction Alberta and the Saskatchewan Research Council, to name a few.

We should point out, though, that not everyone thinks public investment and involvement to spark a green recovery is a good idea.

Chris Ragan, chair of the Ecofiscal Commission, recently warned that “engineering a ‘green recovery’ is a terrible idea.” He suggested that it’s better to just raise the carbon price two- or threefold and let the magic of the invisible hand do its work.

While a carbon tax is part of the policy toolkit, it won’t be sufficient to propel a green recovery at the speed needed. Raising the carbon tax from a dime per litre of gas to 25 cents a litre certainly doesn’t hurt the economics for getting an electric car (EV), but it’s unlikely to be a material inducement, given that EVs already save the average driver more than $1,000 per year on the differential between what it costs to fill up at the pump versus by the plug. A hiked carbon tax would make this a little sweeter, but just by a few hundred dollars.

Raising the carbon tax won’t address the real barriers to EV adoption, which include a lack of charging infrastructure, the need for a national Zero Emissions Vehicle mandate that requires automakers to supply more EVs (a six-month wait is standard for many EV models) and quirks in the auto-leasing market, which discriminate against new EV models by making maximum depreciation assumptions – even though EVs have proven to hold their value just as well as their internal combustion counterparts.

We know that public investment kick-starts markets. In the case of deep retrofits and to get homes off fossil fuel heating, public investment would catalyze a new deep-retrofit renovation industry. Today, it costs more than $40,000 to retrofit a home and make it flood resilient. Research shows that when retrofits are delivered at scale, where work is coordinated over multiple homes in a neighbourhood, these costs can be reduced by half. Once that happens, retrofits become affordable for homeowners. Markets can then take over and public funds are no longer needed.

Information is key to kick-starting all this. That’s why we suggest that first grants and then retrofit mortgage insurance for deep retrofits be delivered by the CMHC in conjunction with chartered banks – so that information promoting retrofits can be integrated into national conversations about the value of Canadian homes. As awareness grows around Canada’s progress toward achieving net-zero emissions by 2050, home buyers will place more value on net-zero homes. Local utilities can be pressed into service to deliver these programs too.

The lion’s share of work to fire up the low-carbon, high-productivity economy comes down to smart regulation (ZEV mandates, building codes and procurement pull policies), along with industrial policy (of the sort that unlocked billions of dollars in the oil sands).

The Business Council of Canada recently issued a statement saying that “for Canada’s recovery plan to succeed, policy makers will need a growth mindset, a singular focus on economic fundamentals and evidence-based approaches to stimulating economic activity.”

We would tend to agree. But let us not lose sight of the most fundamental of the “economic fundamentals”: our economy exists entirely within and is completely dependent on the natural ecosystems in which it is embedded. As go the ecosystems, so goes the economy.

Thanks to innovations that have made low-carbon options the better buy in most cases, the market jury has already issued its verdict: those who have the low-carbon solutions will have the high-performance economies.

The question is this: do we want to be buyers or suppliers for the green economy goods and services that will drive the wealth of nations this century?

If we want to be suppliers, now is the time to pony up.

| Owning the Podium | |||

| LCE growth markets | 2030 Market Opportunity for Canada | Canada’s Competitive Advantage | Explanation |

| Sustainable aviation fuels (SAF) | Medium | High | Abundance of bio-based waste feedstock and industrial fuels infrastructure |

| Carbon fibres/Activated carbon (CFs/AC) | Large | High | Largest feedstock supply for carbon fibres on planet (15-20% of bitumen is carbon fibre feedstock) |

| Low carbon economy minerals and materials | Medium | High | Green grid and leading pilots |

| Batteries | Large | High | Nickel supply well suited + strong petrochemical infrastructure |

| Electric Vehicles (EVs) | Medium-Large | Average | Strong auto-supply chain and promising startups in EV bus and trucks |

| Green hydrogen (H2) | Medium | High | Abundant feedstock, suitable geology for cheap sequestration, pipeline infrastructure |

Postscript: While this series has been largely focused on the green economy elements of a green recovery, we would like to acknowledge that it is unlikely there will be a green recovery unless there is a big-tent coalition that is bold and creative enough to dislodge the forces of inertia. The best chance we have for the green economy to prevail is by marrying the green economy movement with social justice movements, which on a practical level means Building Back Better with vastly enhanced supports for eldercare, childcare and living wages, and as we’ve noted repeatedly throughout the series, by supporting thriving Indigenous communities.

Ralph Torrie is senior associate with Sustainability Solutions Group and partner at Torrie Smith Associates.

Céline Bak is the founder and president of Analytica Advisors.

Toby Heaps is the CEO and co-founder of Corporate Knights.

Notice to reader: Please be aware some of the figures and other details in this white paper have been updated in the Final Report to reflect feedback.