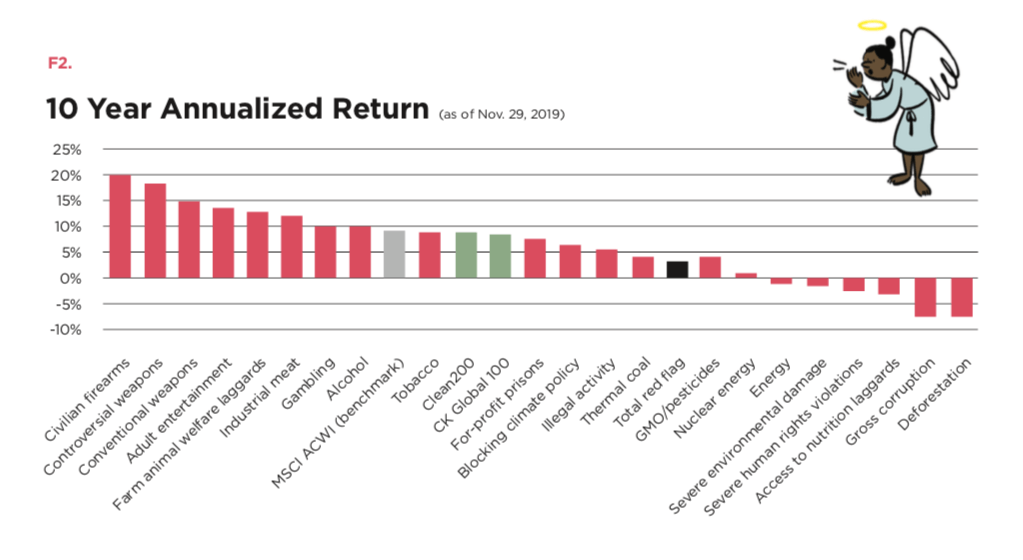

Does it pay to be naughty? It depends on the definition of naughty and which time period. To provide some insight, Corporate Knights used S&P Capital IQ to calculate the 10-year annualized total return (up to Nov. 29, 2019) for 21 red-flag themes.

Over the past 10 years, vice was virtuous for returns if you invested in guns, sex, meat, gambling and booze, all of which outperformed the stock market on average.

That guns are smoking stocks is not surprising, given that military spending, led by the U.S., has been on the rise for the past decade, and given the tragic frequency of mass shootings, which tend to boost sales as gun owners rush to stock up in fear that their right to bear arms will be curtailed.

MindGeek, based in Montreal, has cornered a huge chunk of the pornography market, but it is privately held, so no peeking for public investors. What is left over for public investors are a few piddly stocks that make up 0.02% of the total stock market, but they are grinding out above-market returns.

Owning gambling stocks has been a good bet for the past 10 years, thanks to a booming economy and casino operators expanding in Asia, but it may not pay to “own the house” when the economy hits a downturn.

Plant protein options like Beyond Meat are bursting onto the scene but have yet to take a bite out of surging demand for meat as Asia’s middle class grows. There could be some indigestion for the meat industry as animal welfare and health concerns propel a growing wave of flexitarianism and veganism around the world (which there is now an ETF for, by the way: VEGN is now listed on the NYSE).

Vice was not so nice for returns if you got stuck holding a bag full of companies on the wrong side of the law, human rights or the low-carbon economic transition.

While he is not a tobacco investor himself anymore, Warren Buffett once famously said, “I’ll tell you why I like the cigarette business. It costs a penny to make. Sell it for a dollar. It’s addictive. And there’s fantastic brand loyalty.” But as anti-smoking regulations continue to tighten, tobacco must now share the air with pot and vaping.

Prisons are a captive market, but for-profit prison stocks are getting booked for underperformance in the wake of a backlash from pictures of kids in cages at GEO Group that have been beamed around the world.

Crime has not paid for investors in the 100 companies with the worst records for breaking the law, which have acted as a ball and chain on their returns.

What used to be known as “black gold” is increasingly the source of red in investor portfolios, as the fossil-fuel growth story comes to an end more quickly than almost anyone predicted. While short-term geopolitical events could produce a rally for this sector, the big money is writing off those without a credible plan to transition to the low-carbon economy.

Just four companies dominate the global market for genetically modified seeds and pesticides. Bayer became the biggest company in the space when it swallowed Monsanto whole in 2018. Since then it has had some growing pains, under a heap of lawsuits related to allegations that the company’s glyphosate-based herbicides cause cancer.

Nuclear reactors create energy by splitting atoms, but they have caused many stockholders to split their hairs on account of their tendency to be delivered late and over-budget. Maybe the much-hyped next generation of nuclear reactors will have better luck.

The companies with the worst records for damaging people’s health, propriety, the environment and human rights have turned out to be wronging investors a lot, too, in terms of forgone returns.

The red-flag theme that has delivered the clearest cut to returns, as the Lorax may have predicted, is severe deforestation, where the worst-offending companies have seen their value axed by over 7% a year for the past 10 years.

How would it have worked out for an investor who went all-in on red-flag stocks?

Not so good. A total red-flag portfolio consisting of stocks across all 21 themes would have generated a 10-year annualized return of 3.6%, or less than half the 9.2% posted by the MSCI ACWI, a commonly used stock market benchmark, or the 9.1% tally of the Clean200, the 200 companies that earn the most revenue from providing environmental and social solutions.

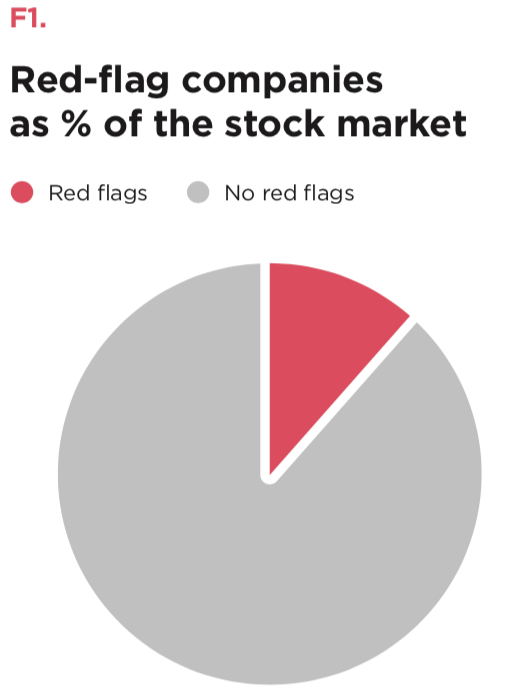

As the next 10 years will likely be different from the last 10 years, perhaps the more important takeaway is that the “baddies” as a group make up a relatively small portion (13%) of the stock market.

So investors can decide which red flags they want to keep out of their portfolios without losing much in terms of diversification.

F1. The list of product/conduct red-flag companies was created by using various reports and databases to determine the “worst-in-class” companies for various indicators. The sources for each indicator are as follows: access-to-nutrition laggards – Access to Nutrition Initiative; blocking climate policy – InfluenceMap; civilian firearms – NZ Super Fund; controversial weapons – Norges Bank Investment Management (NBIM), NZ Super Fund; conventional weapons – Stockholm International Peace Research Institute; deforestation – Chain Reaction Research; farm-animal welfare – Business Benchmark on Farm Animal Welfare; for-profit prisons – American Friends Service Committee; gross corruption violations – NBIM; illegal activity – Corporate Knights Database; severe environmental damage – NBIM; severe human rights violations – NBIM; thermal coal – NBIM; tobacco – NBIM; adult entertainment – Motley Fool, Wespath; alcohol – S&P Capital IQ Industry Classification; energy (fossil fuels) – S&P Capital IQ Industry Classification; gambling – S&P Capital IQ Industry Classification; GMO pesticides – United States Department of Agriculture; industrial meat – Corporate Knights Database; nuclear energy – MVIS Indices.

F2. Total 10-year annualized USD returns for each red-flag category were calculated using S&P Capital IQ. Securities for each red-flag category are weighted according to market capitalization and rebalanced semi-annually. The CK Global 100 Index category was calculated separately by Solactive.